Is Orchard Collection a Good Investment? Honest Analysis for 2026 Buyers

Table of Contents

The most important question any property investor asks is simple: will this make money? In this article, Realtique provides an honest, balanced investment analysis of Orchard Collection for 2026 buyers — covering the macro case for Binh Duong, capital growth drivers from infrastructure, realistic rental yield projections, developer risk assessment, and the risks that balanced investors must acknowledge. This is not a sales pitch. It is the analysis a buyer’s agent would give a serious client. For project specifications, see our complete Orchard Collection guide. For pricing details, see the payment plans breakdown.

The Macro Case for Binh Duong — Why Now?

Vietnam’s GDP growth has consistently ranked among Asia’s strongest over the past decade, averaging 6–7% annually. Binh Duong Province is a core contributor to this growth: it is one of Vietnam’s top three provinces by industrial output, and home to Vietnam Singapore Industrial Park (VSIP) — jointly developed by Vietnam and Singapore, and one of the country’s most successful FDI destinations.

Three macro factors create a compelling investment case for Binh Duong property in 2026:

- FDI inflow growth: Vietnam attracted over USD 36 billion in FDI in 2023. Binh Duong absorbed a significant share through VSIP and surrounding industrial zones, creating sustained expat professional demand.

- Infrastructure uplift: Highway 13 widening to 60m, Ring Road 3, and Metro Line 1 extension (covered in detail in our location and connectivity article) represent a generational infrastructure investment in this corridor.

- Urbanisation and income growth: Vietnam’s middle class is expanding at 1.5–2 million households per year. Binh Duong, as HCMC’s most significant satellite city, captures overflow residential demand from buyers priced out of central Saigon.

This macro backdrop doesn’t guarantee returns on any individual property — but it establishes a fundamentally supportive environment for premium residential investment in the Binh Duong corridor.

Capital Growth Drivers — Infrastructure Creating Value

Infrastructure investment is the most documented driver of residential property value in emerging Asian markets. The mechanism is well-established: reduced commute times → increased desirability of previously peripheral locations → increased demand → price appreciation.

For Orchard Collection specifically, the capital growth drivers are:

| Infrastructure Project | Completion Est. | Expected Impact on Orchard Collection Zone |

|---|---|---|

| Highway 13 widening (60m, 10–14 lanes) | 2026–2028 | Reduced commute to HCMC CBD from 60→35 min; increased corridor desirability |

| Ring Road 3 (Binh Duong section) | 2026–2027 | Direct orbital access to Long Thanh Airport; logistics/expat demand growth |

| Metro Line 1 Extension (Binh Duong) | 2028–2030 | Rail commute to Ben Thanh; transit-oriented premium |

| Long Thanh International Airport | 2026 Phase 1 | Binh Duong as preferred residential zone for regional aviation professionals |

Historical precedent from Vietnamese infrastructure projects: the completion of the Nguyen Van Linh Boulevard in District 7 (2001–2005) correlated with 3–5× residential price growth in adjacent zones over 10 years. The Metro Line 2 corridor in HCMC has already produced 15–20% premiums in transit-adjacent developments. Binh Duong’s infrastructure upgrade is comparable in scale.

Rental Yield Potential — Expatriate Demand in Binh Duong

Rental yield — annual rent divided by purchase price — is the primary income metric for buy-to-let investors. Binh Duong’s rental market is driven primarily by expatriate professionals working in VSIP, Binh Duong New City’s commercial district, and multinational manufacturing operations.

Indicative Rental Range (Projected, 2028–2029)

| Unit Type | Monthly Rent Est. (VND) | Monthly Rent Est. (USD) | Gross Yield (VND basis) |

|---|---|---|---|

| 2BR Large (91 m²) | 18,000,000–25,000,000 | $692–$962 | 3.4%–4.7% |

| 3BR+ Flexible (125 m²) | 25,000,000–35,000,000 | $962–$1,346 | 3.4%–4.7% |

| 4BR Large (157 m²) | 35,000,000–50,000,000 | $1,346–$1,923 | 4.5%–6.4% USD |

Rental estimates are speculative projections for 2028–2029 based on current market comparables and infrastructure projections. They are not guaranteed. The actual rental market at handover will depend on macro conditions, supply levels, and Binh Duong’s economic trajectory over the 2026–2028 period. Buyers must not rely solely on rental projections when assessing affordability.

Why Expatriates Choose Binh Duong — The Rental Demand Driver

Expatriate professionals working in VSIP earn international salaries (USD 3,000–10,000/month depending on role and nationality) and require housing that meets international standards: good security, international school proximity, quality finishes, and lifestyle amenities comparable to Singapore or Bangkok condominiums. Orchard Collection, with its CapitaLand brand, 168 amenities, and Singapore-standard finishing, directly targets this tenant profile — a segment that is currently underserved by existing Binh Duong supply.

Developer Risk Assessment — CapitaLand's Delivery Record

In Vietnam, developer risk — the risk that a project is never completed or is significantly delayed — is a material consideration that buyers must price into their decision. For Orchard Collection, this risk is assessed as low based on the following:

- 32-year Vietnam track record: No project abandoned or buyer deposit lost across the entire CapitaLand Vietnam portfolio

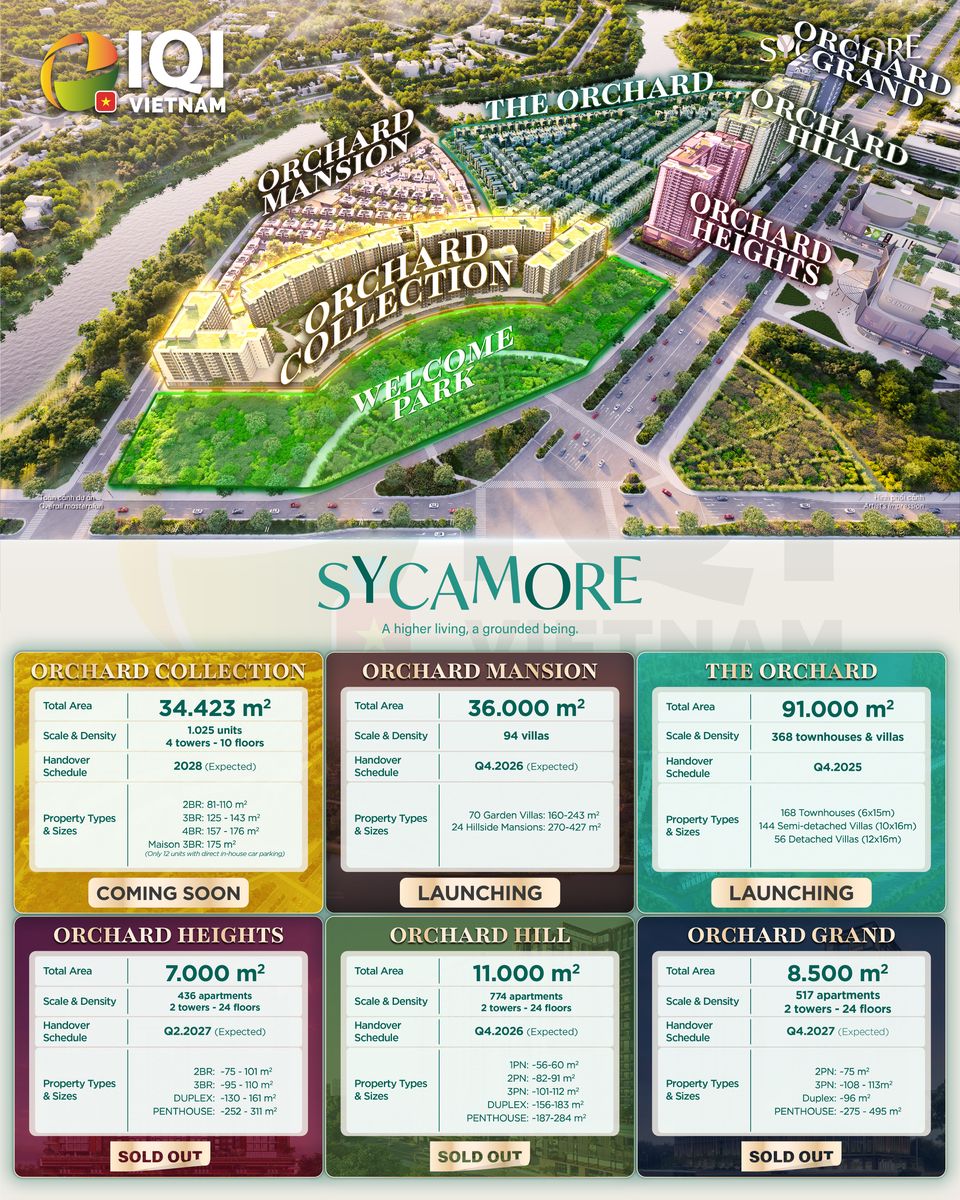

- Five phases of Sycamore delivered: The Orchard, Orchard Hill, Orchard Heights, Orchard Grand, Orchard Mansion — all delivered or in delivery

- Singapore-listed entity: As part of CapitaLand Investment Limited (SGX: CLI), CapitaLand Development operates under Singapore regulatory oversight and financial reporting standards

- Escrow structure: Buyer payments in Vietnam are held in escrow accounts — CapitaLand cannot access funds until specific project milestones are met

- EDGE-certified design: Institutional-grade sustainability certification requires third-party verification, adding accountability layer to construction quality

While no investment is risk-free, the developer risk component of an Orchard Collection investment is materially lower than most Vietnamese domestic developer alternatives.

Risks to Consider — A Balanced View

No investment analysis is complete without acknowledging risks. Orchard Collection buyers should be aware of the following:

- Market timing risk: Property markets can correct. Buying at the Q2/Q3 2026 open sale and holding to Q4 2028 handover — then 2–3 years further for rental maturation — is a 5–6 year capital commitment.

- VND/USD exchange rate risk: For foreign buyers paying in USD, VND depreciation reduces the local-currency equivalent of their investment value. Historical VND depreciation vs USD has averaged 2–3% per year.

- Rental income not guaranteed: Rental projections are indicative only. A significant oversupply of new apartments in Binh Duong between 2026–2028 could compress rental rates.

- Macro Vietnam risk: Vietnam’s property market operates in a regulatory environment that can change — ownership rules for foreigners, capital repatriation, and tax treatment are subject to legislative change.

- Infrastructure delays: Ring Road 3 and Metro Line 1 extension timelines are government targets, not contractual commitments. Delays would reduce the projected commute improvements.

Realtique recommends that investors consult an independent financial advisor before committing to any property purchase in Vietnam. Orchard Collection is a strong product from a credible developer in a growing market — but it is not a guaranteed return investment and should be evaluated as part of a broader portfolio strategy.

Comparison: Orchard Collection vs Keeping VND in Savings

A common alternative investment for Vietnamese buyers is keeping capital in bank savings deposits. The comparison below illustrates why buyers choosing between savings and Orchard Collection are making a meaningful trade-off:

| Metric | Bank Savings (VND) | Orchard Collection |

|---|---|---|

| Annual return (est.) | 6–7% interest rate | 3.5–5% rental yield + capital appreciation |

| Capital security | Government guaranteed (up to VND 125M) | Developer risk — assessed low |

| Liquidity | High — withdraw anytime | Illiquid until handover; resale market then |

| Inflation protection | Limited (VND depreciates) | Real asset; price typically tracks or beats inflation |

| USD-denominated option | No | Yes (4BR + foreign quota) |

| Leverage potential | No | Yes — bank loan up to 70% |

The leverage element is the key differentiator: a buyer who puts VND 3 billion down and borrows VND 6 billion to buy a 3BR+ at VND 8.88 billion total is effectively deploying 3× leverage on their capital — meaning a 10% capital appreciation produces a 30% return on their equity. This magnification works in both directions, which is why risk management and holding capacity are essential to the investment decision.

Note for Foreign Buyers: Bank financing (mortgage loans) for property purchase in Vietnam is only available to Vietnamese citizens. Foreign nationals must fund their purchase through personal capital. The loan-based scenarios above are for Vietnamese buyers only.

Ready to book your unit at Orchard Collection? Realtique is CapitaLand’s authorised selling agent. Contact us for exclusive access, priority booking, and personalised unit recommendations.

📞 Hotline: 0866 810 689 (Mon–Sun, 8AM–9PM)

📧 Email: [email protected]

🌐 Website: realtique.net

Get the Full Orchard Collection Investment Report

A senior Realtique advisor will send you real unit availability, the best unit pick for your budget, and the foreign buyer process — within 24 hours. No spam, no hard-sell.

Fill in the form below — we reply within 24 hours. Or call +84 866 810 689.

{kind=link}

{kind=link}