The Berkley Price 2026 — Foreign vs Vietnamese Payment Tracks Decoded

Table of Contents

The Berkley publishes seven payment schemes — three for foreign buyers, four for Vietnamese — and the headline discount on each ranges from 3 per cent to 17.5 per cent. Those numbers are accurate, but they are not directly comparable. Each scheme has different cash-out timing, different opportunity cost on the deposit, and different exposure to the developer’s milestone risk. The right scheme for you depends less on the headline discount and more on three variables: how quickly you can deploy capital, whether you intend to lease the unit immediately after handover, and whether you are spending VND or converting from USD.

This article walks through every scheme, calculates the effective discount in present-value terms, and identifies which buyer profile each one actually serves.

The Booking Mechanics Common to All Schemes

Every payment scheme begins with the same booking deposit: VND 200 million (approximately USD 8,000 at current rates). The deposit is paid at the point of unit reservation, before the formal Long-Term Lease Agreement (LTLA) is signed.

The deposit is not lost capital. It is credited against the first instalment under whichever payment scheme the buyer ultimately selects. There is a short cooling-off window during which the deposit is refundable; after that, it converts to a binding commitment.

Booking deposit timing matters: in our experience launching prior Sonkim Land projects, the most desirable stacks fill within four to eight weeks of formal launch. With only 85 residences in the entire collection, allocation pressure is real.

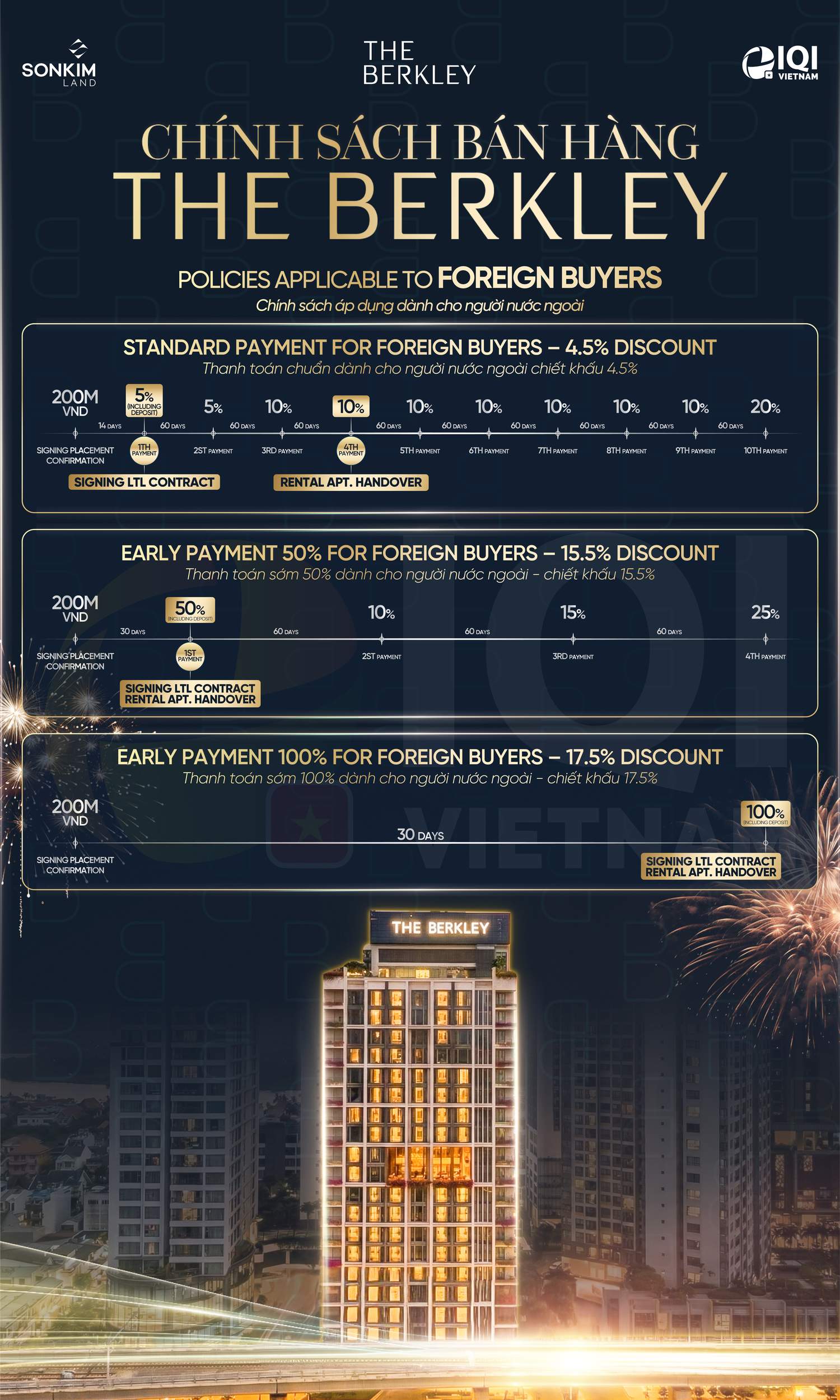

Foreign Buyer Schemes — Three Tracks

Standard Track — 4.5% Discount

The standard track spreads payment across nine instalments, beginning with the booking deposit and a 5 per cent payment on LTLA signing, then 5 or 10 per cent at each subsequent milestone, with the final 20 per cent due at handover.

This is the lowest-discount scheme but the lowest-cash-strain scheme. It works for buyers who want to lock in a unit but spread payments to align with cash flow from elsewhere — typical for expat buyers expecting bonus or carry payments to land within twelve months.

Pros: Smallest upfront cash deployment.

Cons: Smallest discount. The deferred payments do not earn the buyer any return.

Early 50% Track — 15.5% Discount

The Early 50% track requires the buyer to pay 50 per cent of the unit value early in the schedule (booking + LTLA + accelerated milestones), then the remaining 50 per cent staggered through to handover. The discount jumps to 15.5 per cent.

This is the scheme most foreign buyers select. It captures the bulk of the available discount without requiring full upfront payment, and the math comes out clearly favourable in any reasonable cost-of-capital scenario.

Pros: 11-percentage-point discount uplift versus Standard, in exchange for accelerating roughly 35 per cent of payments by twelve to eighteen months. At any cost of capital below ~18 per cent annualised, Early 50% dominates Standard.

Cons: Requires the buyer to be liquid for the early payment milestones. Locking up 50 per cent of unit value reduces optionality.

Early 100% Track — 17.5% Discount

Pay the full unit value up front at LTLA signing, in exchange for the maximum 17.5 per cent discount. Receive the unit at handover.

The 2-percentage-point uplift over Early 50% is the marginal compensation for the additional 50 per cent of capital being deployed earlier.

Pros: Maximum discount. Cleanest paperwork.

Cons: The marginal 2-point pickup is small relative to the additional capital commitment. Unless the buyer has cash earning sub-5 per cent yield elsewhere, Early 50% is mathematically more efficient. Early 100% makes sense primarily for buyers paying from already-low-yielding cash positions, or for paperwork minimalists.

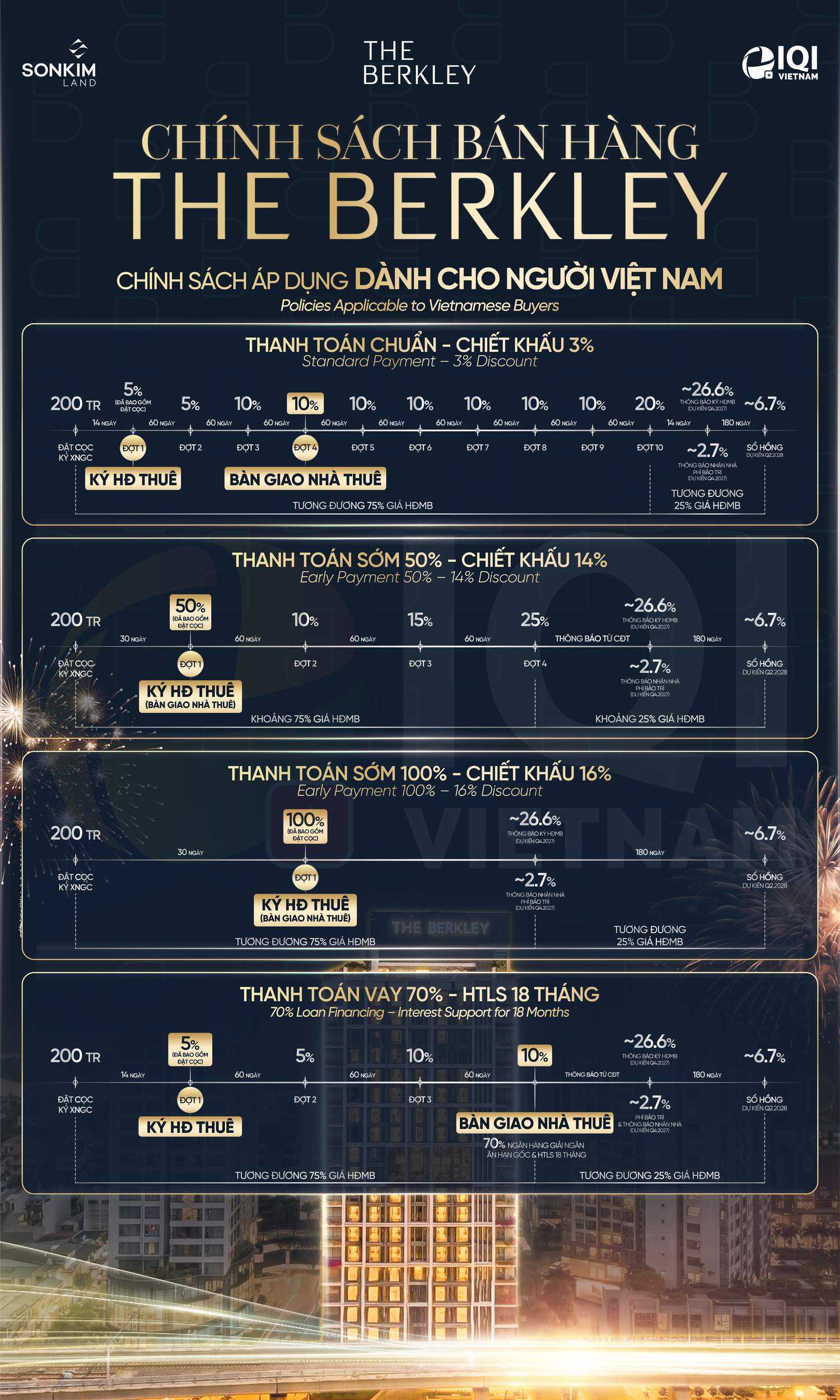

Vietnamese Buyer Schemes — Four Tracks

The Vietnamese-buyer schedule mirrors the foreign one with one structural addition — a fourth track using bank financing.

Standard 3% / Early 50% 14% / Early 100% 16%

Same nine-instalment structure as the foreign tracks, with each headline discount 1.5 percentage points lower. The 1.5-point gap reflects the developer’s commercial preference for filling foreign allocations faster.

The same logic applies in present-value terms — Early 50% remains the dominant scheme for Vietnamese buyers paying from cash. Early 100% is a marginal pickup not worth the additional capital lock-up unless the alternative yield on cash is very low.

70% Loan + 18-Month Interest Support (HTLS) — Vietnamese Only

This is the structurally interesting scheme for Vietnamese investors. Sonkim Land partners with banks to offer a 70 per cent loan at preferential rates, with the developer subsidising interest payments for the first 18 months (“Hỗ Trợ Lãi Suất” / HTLS).

Mechanics: Buyer pays approximately 30 per cent of unit value upfront from cash, plus closing costs. The remaining 70 per cent is bank-financed. For 18 months following handover, the buyer’s interest cost is effectively zero (covered by developer subsidy). After month 18, interest reverts to the prevailing bank rate (currently 10–12 per cent).

This scheme is ideal for yield-focused investors who plan to lease the unit immediately and use rental income to service the loan from month 19 onwards. The trade-off: refinancing risk needs explicit planning.

The Math: Present-Value Comparison

Headline discounts are not directly comparable because each scheme has different cash-flow timing. The right way to compare is present value — discounting each scheme’s payments back to today using the buyer’s cost of capital.

Worked example: hypothetical USD 600,000 (~VND 15 billion) two-bedroom unit, foreign buyer, 8-year hold.

| Scheme | Headline discount | Effective price (PV at 8% cost of capital) | IRR uplift vs baseline |

|---|---|---|---|

| Foreign Standard 4.5% | 4.5% | ~USD 580,500 | (baseline) |

| Foreign Early 50% | 15.5% | ~USD 532,800 | +9.0% IRR |

| Foreign Early 100% | 17.5% | ~USD 525,000 | +1.5% IRR over Early 50% |

Conclusion: Early 50% is the clear winner for any foreign buyer with cost of capital between 5–12 per cent. Early 100% becomes attractive only at cost of capital below 4 per cent.

What the Brochure Doesn't Tell You

1. Stack-level price variation can exceed scheme-level discount differences

Within the same unit type, units on different floors and stacks vary in price by 8–15 per cent. Floor level (premium tends to start above level 12), view (river vs city), and metro-side vs courtyard-side orientation all drive this variation. Choosing the right stack within your preferred unit type can save more than choosing between Early 50% and Early 100%.

2. Maintenance fee structure

The Berkley’s monthly maintenance fee sits at the high end of HCMC luxury — a function of the small resident base supporting the rooftop pool, gym, yoga, lobby concierge, and 24/7 security. Budget approximately VND 18,000–22,000 per square metre per month (~USD 0.75–0.90/sqm/month). For a 100 sqm unit, this is USD 75–90 per month, or ~USD 1,000 per year.

Material for yield calculations: a 5 per cent gross rental yield becomes a 4 per cent net yield after maintenance, before tax.

3. Furnishing budget

The Berkley delivers fully completed but unfurnished. Budget USD 25,000–60,000 for furnishing depending on style and quality preference. Recoverable through rental premium if leased furnished, but a real near-term cash requirement that buyers commonly under-budget.

Which Scheme Suits Which Buyer

| Buyer profile | Recommended scheme |

|---|---|

| Foreign expat, salary + bonus inflows, 6–12 month payment horizon | Foreign Standard 4.5% |

| Foreign investor, liquid cash, optimising NPV | Foreign Early 50% 15.5% (default) |

| Foreign investor, very low-yield cash, paperwork minimaliser | Foreign Early 100% 17.5% |

| Vietnamese cash buyer | Vietnamese Early 50% 14% (default) |

| Vietnamese investor levering for yield | Vietnamese 70% Loan + HTLS |

Bottom Line

For 80 per cent of buyers, the Early 50% scheme — foreign or Vietnamese — is the right answer. The Standard scheme is a cash-flow accommodation, not an optimisation. The Early 100% scheme is a marginal 2-point uplift in exchange for substantial additional capital commitment, which only makes sense for buyers with low alternative yield. The Vietnamese 70% Loan + HTLS scheme is the most structurally interesting for yield-focused investors but introduces refinancing risk after month 18 that needs explicit planning.

Whichever scheme you choose, the booking deposit math is the same — VND 200 million holds the unit, refundable inside the cooling-off window, and credited against your first instalment thereafter.

Get the Full The Berkley Investment Report

Pricing by stack and floor · Payment track comparison · Lease structure summary for foreign buyers

Only 85 residences. Allocations move fast. Drop your details below — we will send you the live availability map, payment-scheme math run on your entry size, and a private walkthrough invitation within the same working day. Or speak directly: +84 866 810 689.

KC Pham

More on The Berkley Thao Dien

- ★ Complete Review 2026 (Pillar)

- → Thao Dien: Vietnam’s #1 International Enclave

- → An Phu Metro & The TOD Effect

- → Floor Plans: 13 Layouts Decoded

- → Amenities + Thao Dien Hotspots

- → Is The Berkley Overpriced?

- → Long-Term Lease Structure

- → Buyer’s Guide A-Z

- → Insider’s Decision Guide

- → Sonkim Land Track Record